- State Bank of India (SBI)

- Indian Bank

- Canara Bank

- Punjab National Bank

- Bank of Baroda

- Bank of Maharashtra

- Central Bank of India

- Stamp Duty: 0.5% of the loan amount Rs.42,500

- Registration Fee: 0.1% of the loan amount Rs.8,500

- Total Cost: Rs.51,000

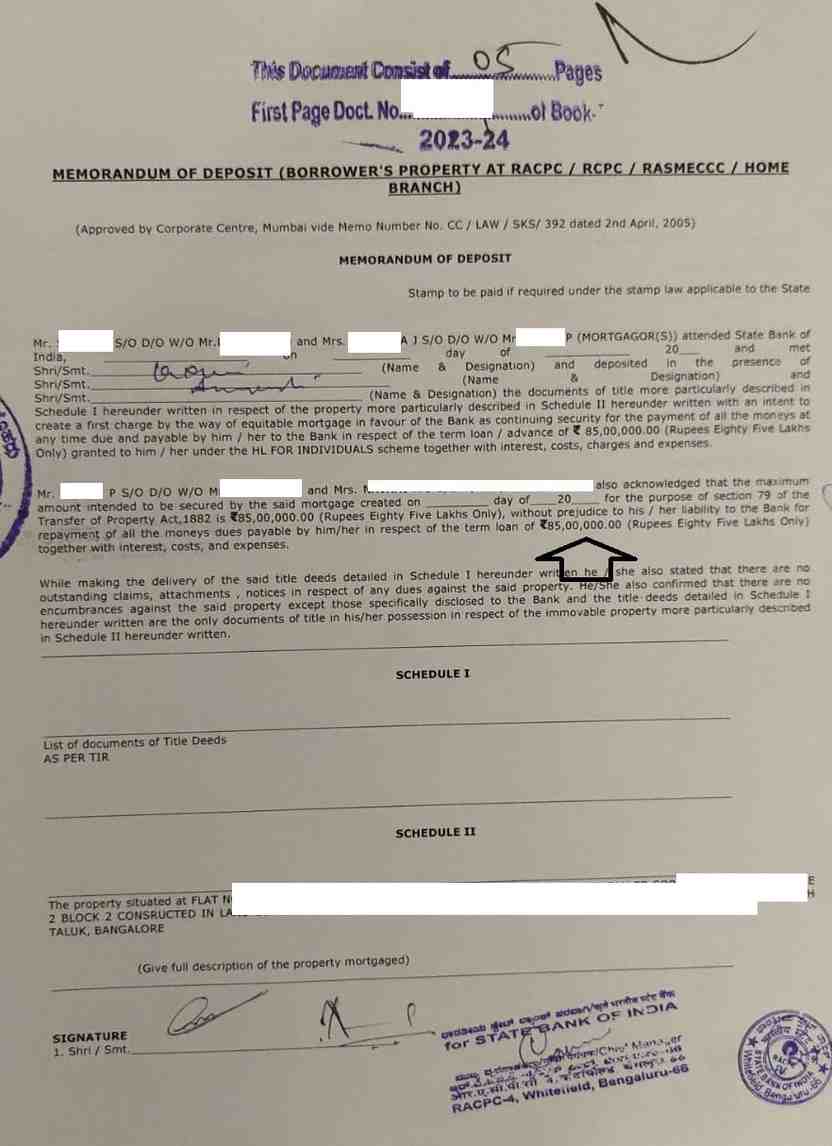

Despite requesting SBI to waive the registration requirement, the bank insisted on completing the process. In our experience, public sector banks seldom allow the borrower to skip mortgage registration.

Despite requesting SBI to waive the registration requirement, the bank insisted on completing the process. In our experience, public sector banks seldom allow the borrower to skip mortgage registration.

PRIVATE SECTOR BANKS – CONDITIONAL OR NO REGISTRATION In contrast, many private sector banks and housing finance companies require mortgage registration only if the loan amount exceeds Rs.1 crore. Based on our personal case handling, the following lenders have not mandated mortgage registration for loans below ₹1 crore:

- HDFC Bank Ltd

- ICICI Bank Ltd

- Axis Bank Ltd

- LIC Housing Finance Ltd

WHY DO SOME BORROWERS INTENTIONALLY AVOID REGISTRATION? Some borrowers may consciously avoid mortgage registration for the following reasons:

- Cost Saving – To avoid paying stamp duty and registration fees.

- Privacy – Since an unregistered mortgage does not reflect in the Encumbrance Certificate, the loan remains out of public records.

CONCLUSION Whether or not mortgage registration is required depends on three main factors:

- The bank or lending institution you choose,

- The loan amount, and

- The internal policy of the lender.

- Public sector banks typically mandate mortgage registration.

- Private sector banks may waive registration for loan amounts below Rs.1 crore.

- For loans above Rs.1 crore, registration is almost always required regardless of the lender.

- Email: pgnproperties@gmail.com

- WhatsApp: +91-97424-79020