In our recent transaction, we implemented a dual-agreement strategy for purchasing a flat, executing separate agreements for the property and furniture & fixtures. This approach offers financial flexibility and customized loan structuring.

Let me share the context for better understanding

CASE BACKGROUND

One of my clients was selling a 2BHK flat in Bangalore. The guidance value of the property was Rs 40.80 Lakhs. The buyer agreed to purchase the flat at Rs 41 Lakhs, which was in line with the guidance value.

However, the seller had made substantial investments in high-quality furniture and fittings. He was keen on recovering this investment and quoted an additional Rs 28 Lakhs for these items.

Typically, property and furnishings are combined into a single sale agreement for resale property, especially when a home loan is involved. However, in this case, we opted to structure the transaction through two separate agreements. We also consulted with the bank, which approved the arrangement and sanctioned two distinct loans: one for the property and another for the furniture.

EXECUTION OF AGREEMENTS

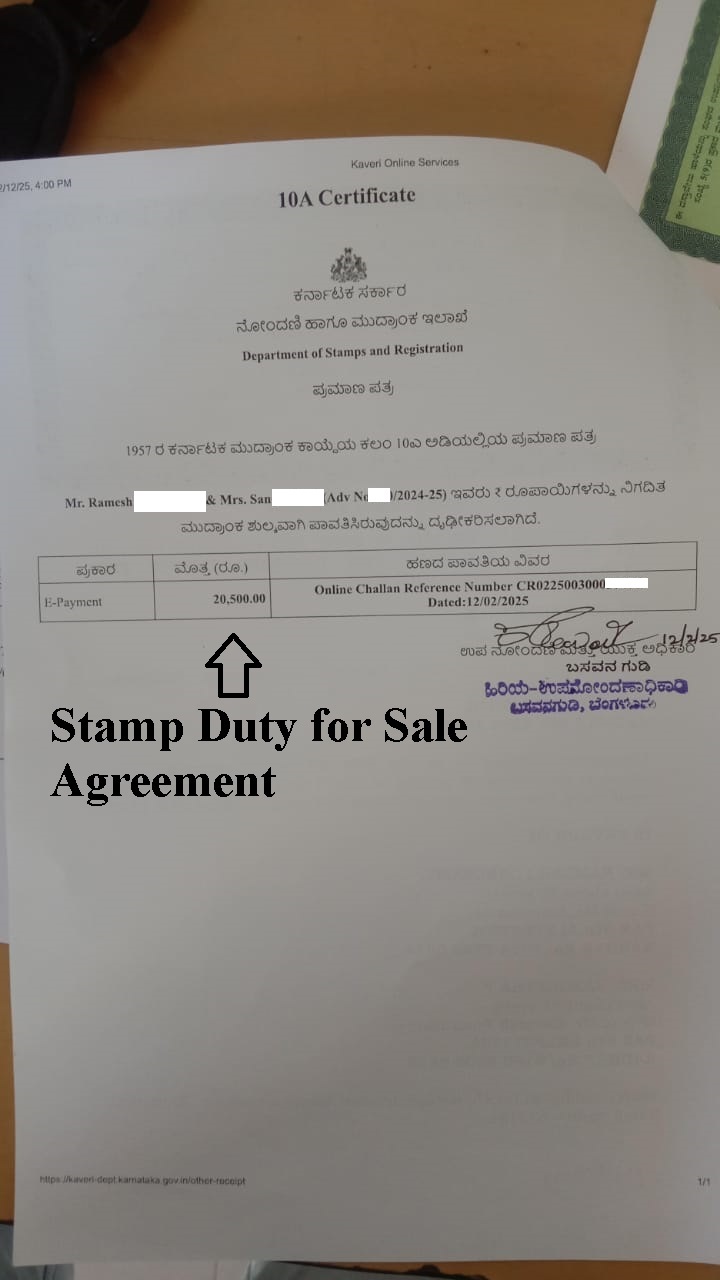

- Property Sale Agreement:

We first expected the Sale Agreement for the flat, reflecting the property value at Rs. 41 Lakhs. The applicable stamp duty for this agreement was 0.5%, amounting to Rs. 20,500

Refer to the below adjudication

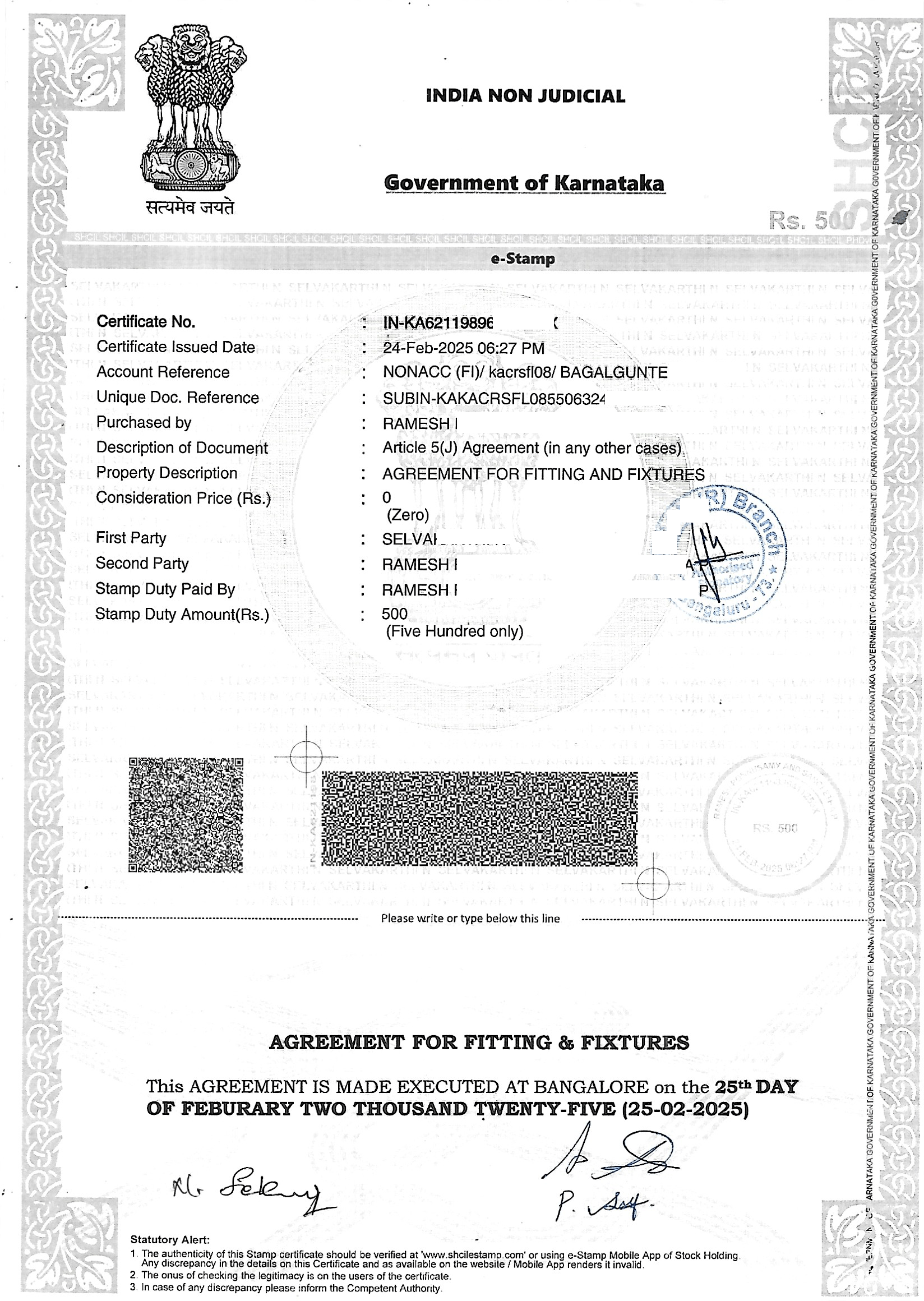

- Furniture & Fixtures Agreement

Next, we executed a separate agreement for furniture and fittings on a non-judicial e-stamp paper. The applicable stamp duty for this agreement was Rs. 500. (The bank provided the standard format for this agreement)

Refer to the below image

LOANS SANCTION

Within a week of executing the above agreement, both loans were sanctioned:

- Property Loan: Rs. 36.90 Lakhs sanctioned against a purchase value of Rs. 41 Lakhs. Refer to the Demand Draft image below

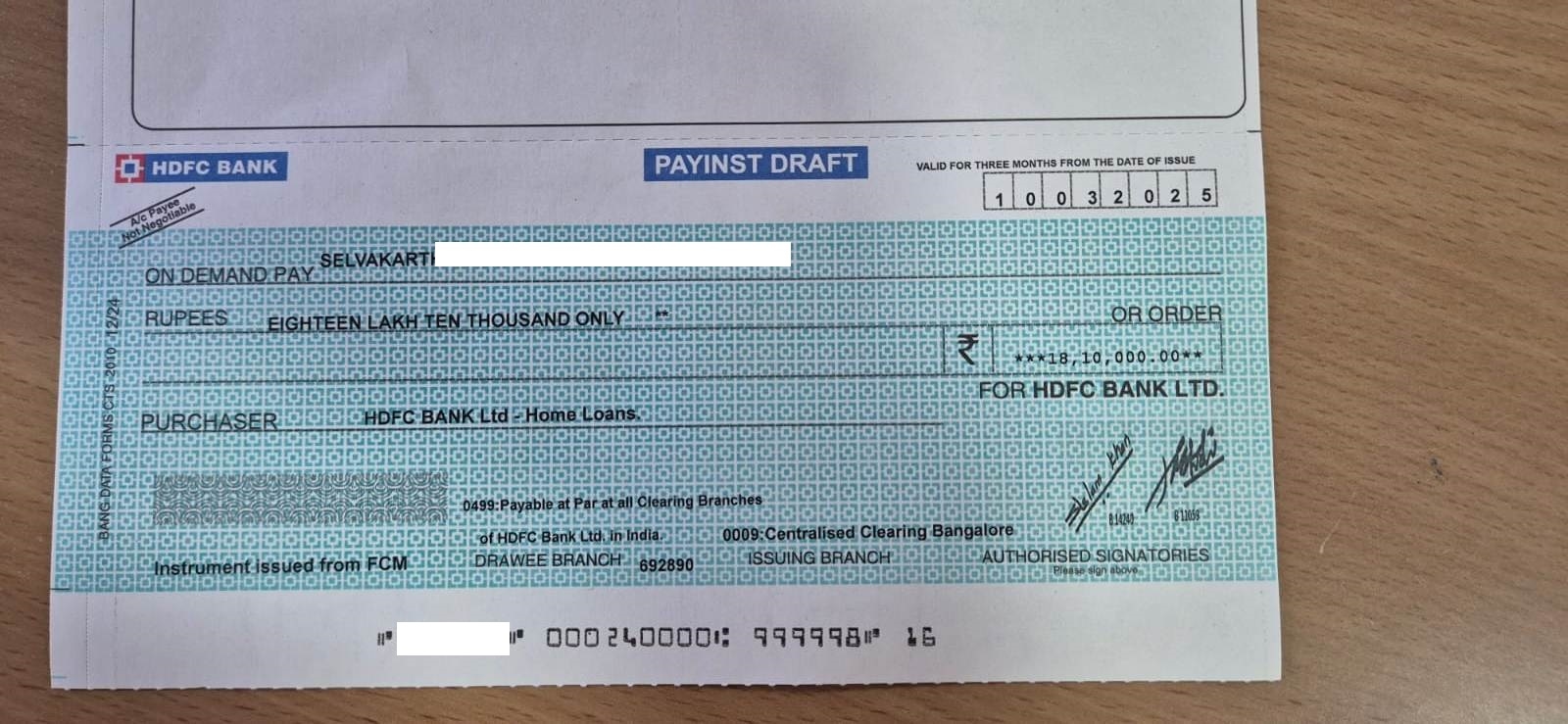

- Furniture Loan: Rs. 18.10 lakhs sanctioned against a value of Rs. 28 lakhs. Refer to the Demand Draft image below

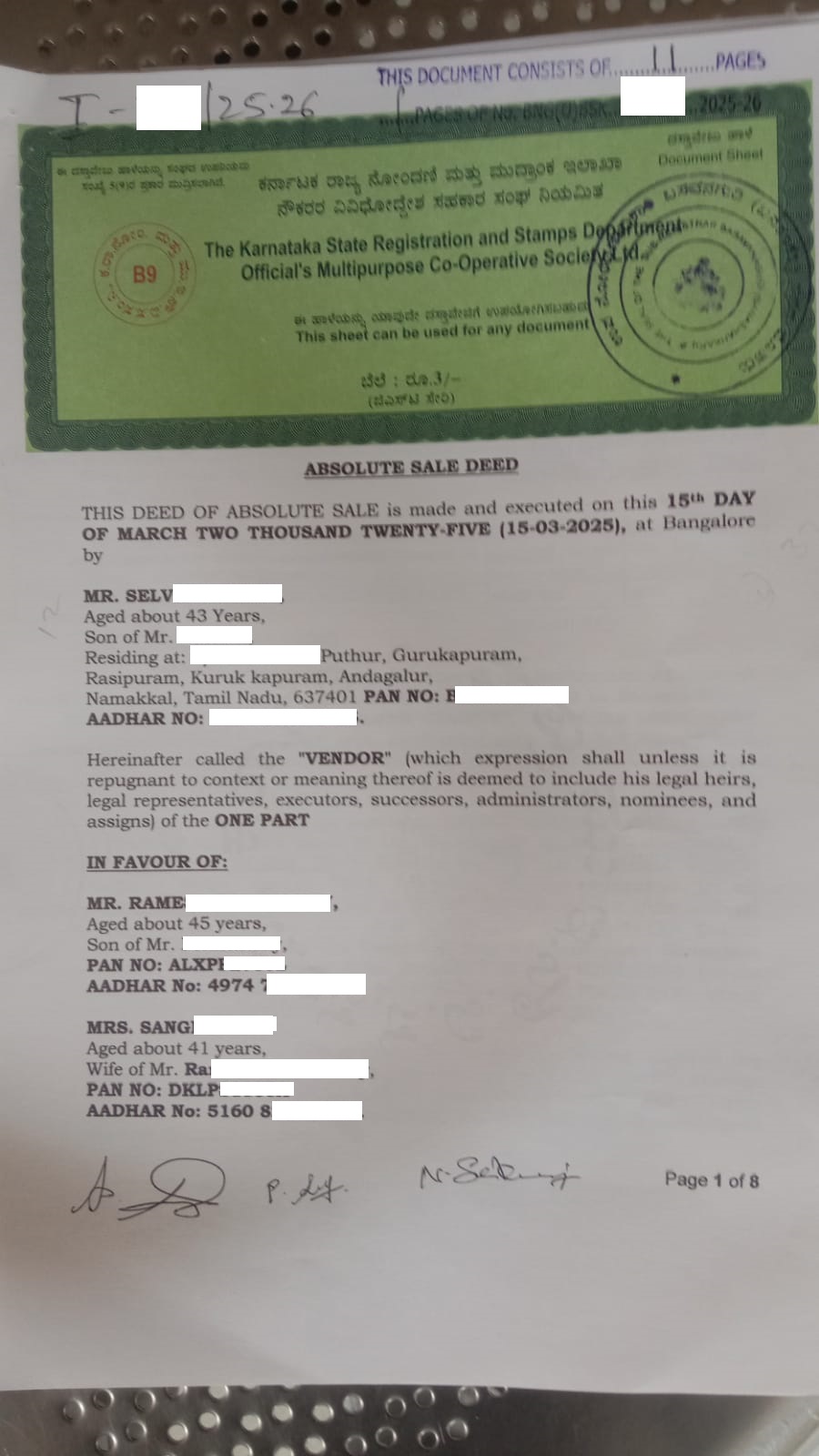

DEED REGISTRATION

We registered the Sale Deed for the Property; refer to the below registered Deed

MODT (MEMORANDUM OF DEPOSIT OF TITLE DEED)

In my case, HDFC did not register the MODT and simply collected the original title document as security. However, banks such as SBI or LIC Housing Finance typically combine both loans and register a single MODT for the total loan amount (including furniture).

- MODT Charges: 0.6% of the loan amount

- MODT should ideally be registered immediately after the sale deed registration (preferably back-to-back registration)

DEMAND DRAFT (DD) HANDOVER:

- During the Sale Deed Registration, the bank’s representative was present at the sub-registrar office with both DDs

- After registration, the representative collected the title documents, simultaneously handing over both DDs to the seller.

CONCLUSION

Implementing a dual-agreement strategy — one for the property and another for the furniture & Fixtures can offer greater financial flexibility. However, inbuilt furniture may be considered an integral part of the property and might not qualify for separate documentation. It is essential to consult with your bank and legal advisor to ensure proper documents and compliance.

NEED ASSISTANCE? WRITE TO US

Email: pgnproperties@gmail.com

Contact or WhatsApp: +91-9742479020