Before answering how to find if a property is mortgaged and with which bank, it is essential to understand the two types of property mortgages in India. This foundational knowledge will provide a comprehensive view of how mortgage details are recorded and verified.

Types of Property Mortgage

Mortgages in India are broadly classified into two categories:

- Registered Mortgage

- Equitable Mortgage

- REGISTERED MORTGAGE

A Registered Mortgage is documented at the Sub-Registrar Office or with a designated government agency. The details are officially recorded and publicly accessible.

For instance, in India, registered mortgage data is maintained by the Stamps and Registration Department of the respective state. This information is reflected in the Encumbrance Certificate (EC), which can be extracted online in many states.

Most public sector banks in India prefer registered mortgages as it provides them with a clear legal standing in case of borrower default.

Closure of Registered Mortgage:

Once the loan is repaid, the borrower can register a Deed of Reconveyance to remove the mortgage lien from government records.

- EQUITABLE MORTGAGE

An Equitable Mortgage involves the borrower depositing the original title documents with the lender as security for the loan. This type of mortgage is not registered with any government authority and therefore is not reflected in the Encumbrance Certificate.

Equitable mortgages are typically used by private lenders and banks.

Closure of Equitable Mortgage:

After the loan is repaid, the lender issues a No Objection Certificate (NOC) and returns the original title documents to the borrower.

HOW TO VERIFY IF A PROPERTY HAS A MORTGAGE

Here are three reliable methods to determine if a property is under mortgage and with which bank:

- Extract the Encumbrance Certificate (EC)

The EC provides a record of all registered transactions related to a property, including sale, gift, lease, and mortgage.

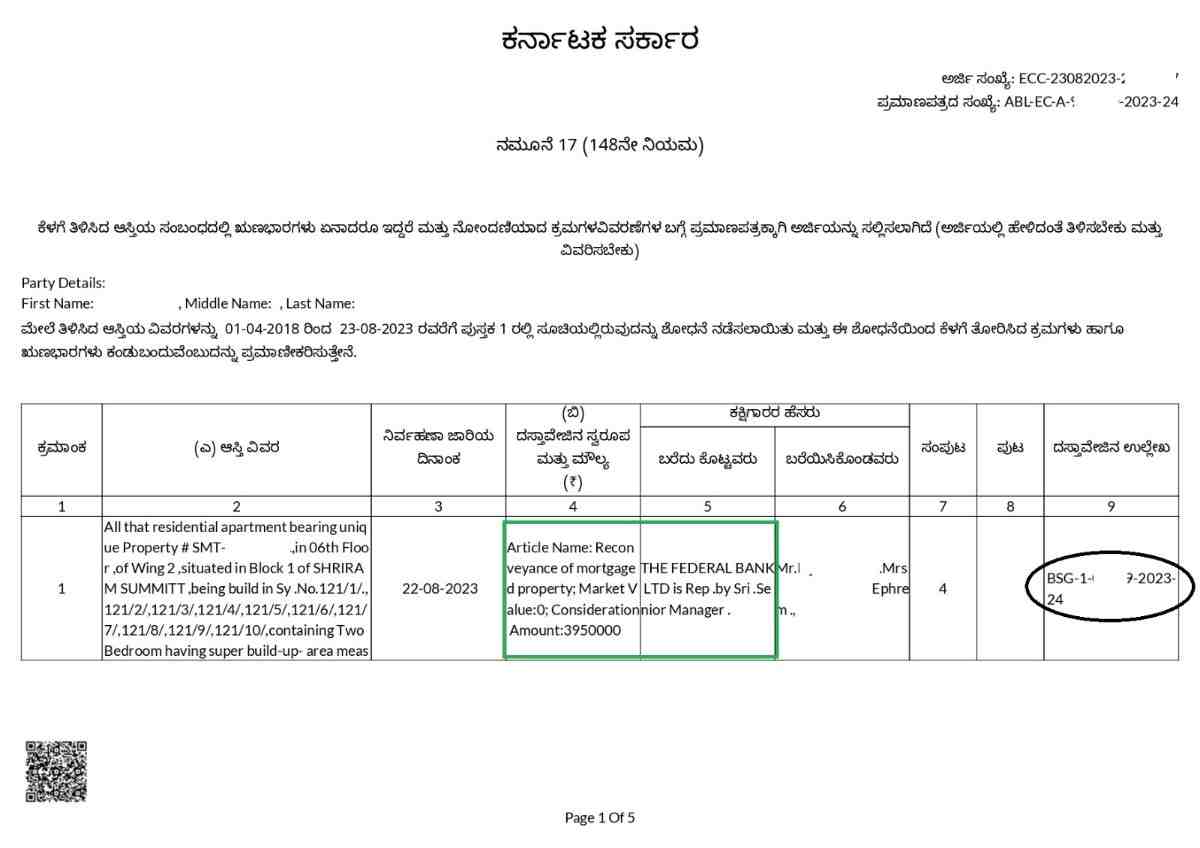

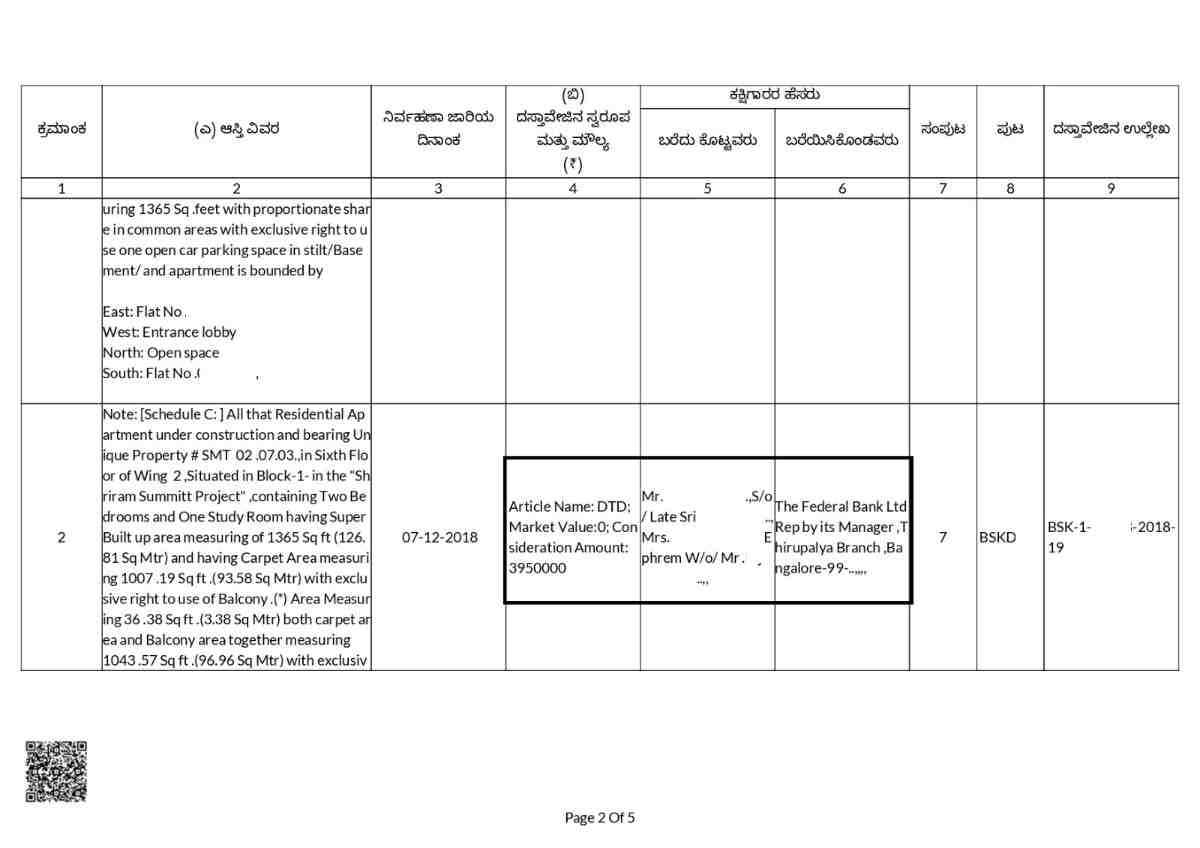

Example Case:

Suppose you wish to purchase a resale flat in Bangalore. Before proceeding, it’s crucial to check if any mortgage exists. To do this, we extracted the EC from Kaveri Online Services. Refer to below EC

From the EC:

- Serial No. 2 dated 07-12-2018: Shows a mortgage of Rs.39,50,000 with The Federal Bank Ltd. (highlighted in black in the image).

- Serial No. 1 dated 22-08-2023: Indicates repayment of the mortgage and registration of the Reconveyance Deed (highlighted in green).

- Verify the Original Title Documents

If the EC does not reflect any mortgage, the next step is to request the original title documents from the seller. Key documents include:

- Sale Deed

- Parent Deed

- Tax Receipts

- eKhata

Sellers often hesitate to share originals, fearing misuse. In such cases, request to inspect the originals in their presence and return them immediately after verification.

NOTE: If the seller holds the original documents, it is a strong indication that the property is not mortgaged. Conversely, refusal or inability to produce them could imply the presence of an equitable mortgage.

If an equitable mortgage existed, ensure the seller provides the No Objection Certificate (NOC) from the lender.

OUR ASSISTANCE

We provide professional assistance in extracting Encumbrance Certificates and verifying property mortgage

To avail our services, please contact:

- Email: pgnproperties@gmail.com

- WhatsApp: +91-97424-79020

FAQ: CHECKING IF A PROPERTY HAS A MORTGAGE & IDENTIFYING THE BANK

Q1. Why is it important to check whether a property has a mortgage before buying it?

Answer:

- To ensure there are no hidden liens or encumbrances that may cause legal or financial liability.

- To make sure the seller has clear title and the right to sell.

- To avoid having to pay off someone else’s loan unexpectedly.

- To negotiate terms or price appropriately, or demand a “No Objection Certificate” or clearance if a loan existed.

Q2. What documents or records should I request from the seller?

Answer:

Some of the key documents are:

- Title deed(s) / sale deed(s)

- Encumbrance Certificate (EC) for relevant years

- Possession certificate, if applicable

- Previous mortgage or loan clearance documents (if they had financed earlier)

- No Objection Certificate (NOC) from the bank (if a mortgage had existed)

- Any documents indicating that the loan has been fully repaid and released

Q3. What is an Encumbrance Certificate (EC), and how does it help?

Answer:

An Encumbrance Certificate (EC) is an official record issued by the sub-registrar’s office which shows whether any transaction (sale, mortgage, lien, etc.) is recorded against a property over a given period.

If a mortgage or loan was registered, it should appear in the EC for the relevant years.

An EC effectively helps you trace all legal and financial encumbrances on the property over a period.

Q4. How can I find which bank or financial institution holds the mortgage on a property?

Answer:

- The EC may list the mortgage transaction, sometimes mentioning the mortgagee (bank).

- The seller should provide the loan documents or statements showing the bank name.

- The bank’s NOC (if issued) will name the lender.

- In some jurisdictions, government public search portals can show the details of registered mortgages (e.g. CERSAI in India).

- In some cases, the sub-registrar office may keep records of the mortgage registration and disclose the mortgagee.

Q5. What if the mortgage has already been paid off — how can I confirm that the bank has released the lien?

Answer:

- Ask the seller for a No Objection Certificate (NOC) or Discharge / Reconveyance Deed from the bank confirming the mortgage has been discharged.

- Check the EC records after the date when the mortgage was repaid;

- Verify with the bank (if known) that the account is closed and no security interest remains.

- In many places, the sub-registrar’s records or relevant public registry should note the “Discharge / Reconveyance Deed” entry.

Q6. What are the limitations or challenges in this verification process?

Answer:

- Some encumbrances might be missing or improperly recorded due to clerical or registration lapses.

- EC may not cover every year unless the request period is sufficiently long.

- Mortgages not registered in the public registry (if legally required but not done) may not show up.

- Seller or bank may delay or refuse to provide necessary clearance documents.

- Regional/local procedural differences may apply depending on the state or jurisdiction.

Q7. If I find there is a mortgage, what precautions should I take before proceeding?

Answer:

- Insist that the seller clear the mortgage fully and deliver NOC / Discharge Deed / Reconveyance Deed documents before or at closing.

- Ideally, structure the payment so that the outstanding balance is paid directly to the bank as part of the transaction.

- Consider holding some portion of the consideration in escrow until all clearances are verified.

- Have your lawyer or legal representative validate all documents and ensure registration of the Discharge / Reconveyance Deed of the lien.

- Only proceed if you are convinced that title is clean and free of hidden liabilities.