A Reconveyance Deed is a legal document that transfers the title of a property back to the borrower from the bank or mortgage lender once the home loan is fully repaid. In simple terms, it removes the “charge” or lien created by the Memorandum of Deposit of Title Deed (MODT) and restores complete ownership rights to the borrower.

If you have taken a loan against your property and executed a MODT with the bank, registering a Reconveyance Deed is a crucial final step after loan closure. Without this step, your property will still appear as mortgaged in the Encumbrance Certificate (EC), which can create problems in future property transactions.

DOCUMENTS ISSUED BY THE BANK AFTER LOAN CLOSURE

Once you have paid the full and final settlement of your loan dues, the bank issues the following documents to proceed with Reconveyance registration:

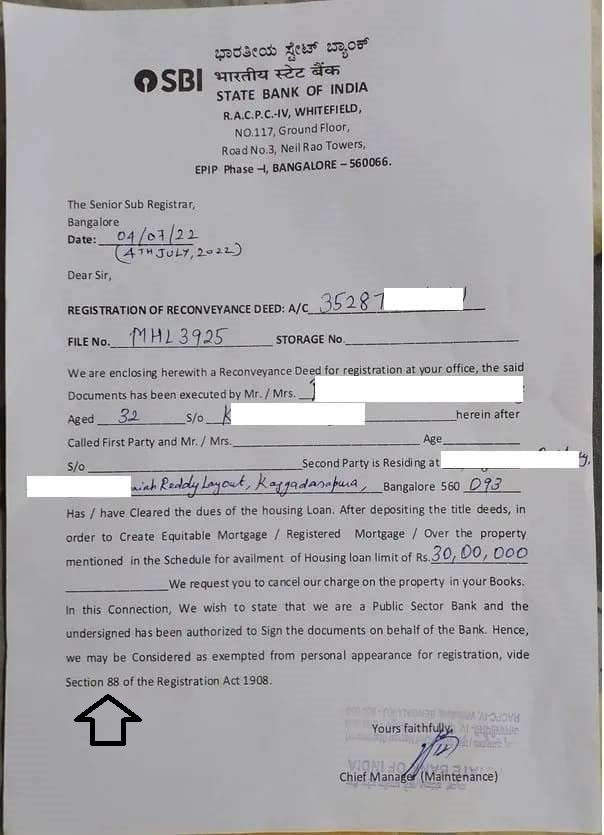

- Exemption Letter – A letter permitting you to register the Reconveyance Deed at the sub-registrar’s office. The presence of a bank representative is not required if this letter is issued. We highlighted the exemption part in below image

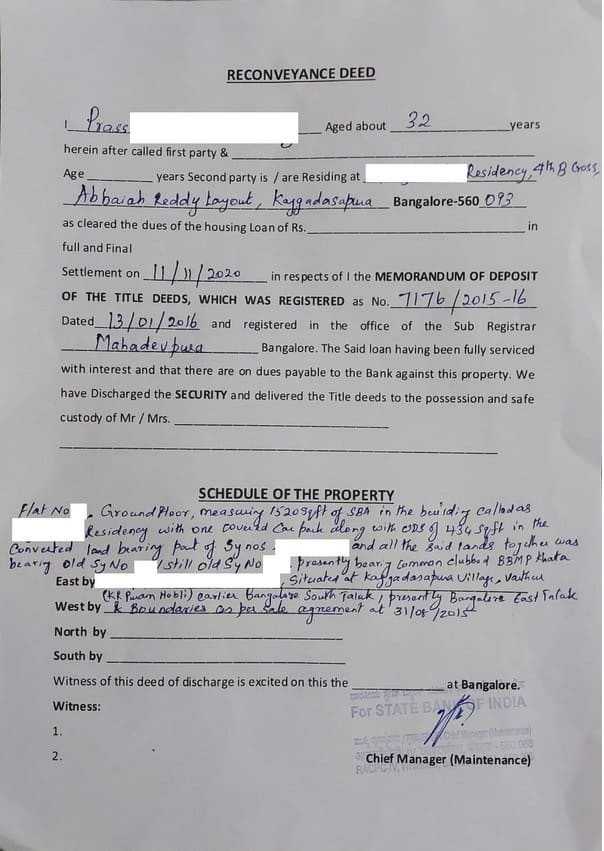

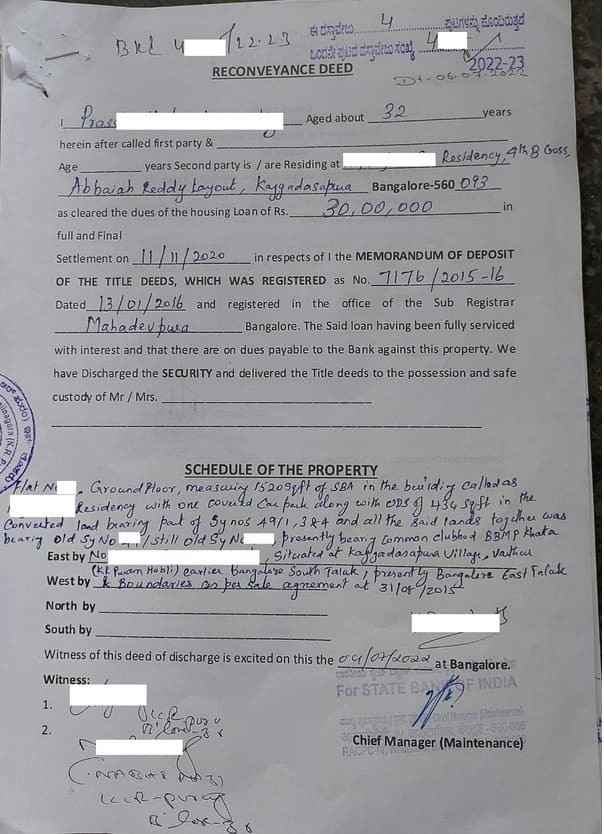

- Reconveyance Deed – A formal deed executed by the bank confirming that the mortgage is satisfied. Refer to below Reconveyance

- Title Documents – The set of original documents you had deposited with the bank at the time of MODT registration (such as sale deed, previous title deeds, khata, etc.).

EXAMPLE CASE STUDY: MY RECONVEYANCE DEED REGISTRATION

To make the process easier to understand, let me share a real-life example of my own experience.

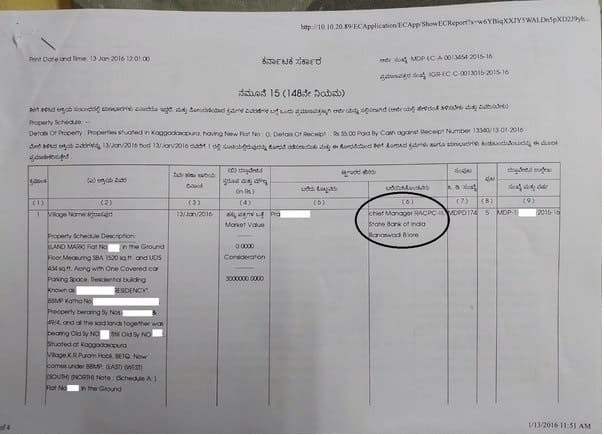

- On 13th January 2016, we registered the MODT with the State Bank of India (SBI) at Mahadevapura Sub-Registrar Office, Bangalore.

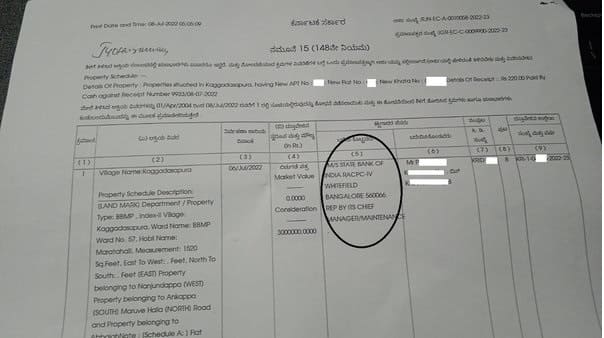

- In the Encumbrance Certificate (EC), Column 5 shows the executor’s name (borrower), and Column 6 shows in whose favor the deed is executed (bank). So, during MODT registration, my name appeared in Column 5, and SBI’s name appeared in Column 6. Refer to below EC

After clearing the loan:

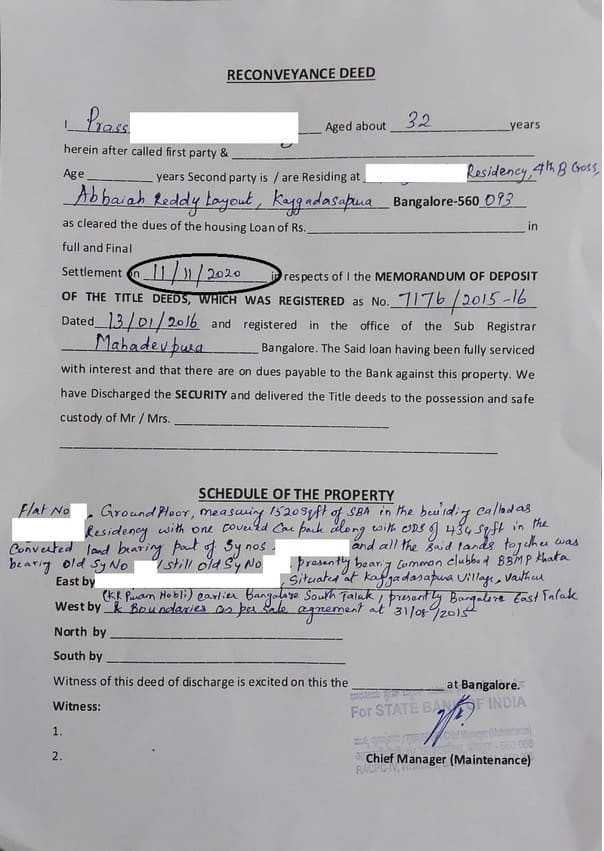

On 11th November 2020, we paid the full and final settlement of our MODT dues. We highlighted the settlement date in below Reconveyance Deed

On 6th July 2022, we collected the following documents from SBI RACPC (Retail Asset Central Processing Centre):

- Exemption Letter

- Reconveyance Deed

- Title Documents

GOVERNMENT CHARGES PAID FOR RECONVEYANCE REGISTRATION (KARNATAKA)

- Stamp Duty – Rs.200

- Registration Fee – Rs.200

- Scanning Charges – Rs. 50 per page (Rs.300)

- Total Cost – Rs. 700

REGISTRATION AT SUB-REGISTRAR OFFICE

On 6th July 2022, we visited K.R. Puram Sub-Registrar Office with:

- Exemption Letter

- Reconveyance Deed issued by the bank

- Aadhaar card (borrower identity proof)

- Payment receipt (K2 Challan)

After registration, the Reconveyance Deed was officially recorded. Refer to the Reconveyance Deed after registration

We applied for the latest EC. In the new Encumbrance Certificate:

- Column 5 showed the Bank’s name (as executor).

- Column 6 showed my name as the buyer.

This confirmed that the mortgage lien had been removed, restoring my property’s clear title. Refer to the EC image

IMPORTANT NOTES ON RECONVEYANCE DEED REGISTRATION

- Reconveyance Deed is applicable only if MODT was registered with the bank. If the bank only collected your documents without MODT registration, simply collect your documents after closure.

- The Reconveyance Deed must be registered in the same Sub-Registrar Office where the MODT was originally registered.

- 90-day rule: The deed should be registered within 90 days of issuance. If the validity lapses, request a fresh Reconveyance Deed from the bank.

- Owner’s presence is mandatory at the sub-registrar office. The bank representative’s presence is not required if the exemption letter is provided.

- If you are abroad or unavailable, you can appoint a Power of Attorney (POA) holder to collect documents and register the Reconveyance Deed.

- After registration, always extract the latest EC to confirm that the bank’s name has been removed.

FAQS ON RECONVEYANCE DEED IN KARNATAKA

1. What is the purpose of a Reconveyance Deed?

A Reconveyance Deed formally removes the mortgage charge from property records and restores full ownership rights to the borrower after loan repayment.

2. Is Reconveyance required if my bank did not register MODT?

No. If the bank only collected documents without MODT registration, simply collect your documents after closing the loan. Reconveyance is not applicable.

3. What happens if I don’t register the Reconveyance Deed?

Your property will still appear as mortgaged in the Encumbrance Certificate. This can cause issues when selling or mortgaging the property in the future.

4. Who should be present during Reconveyance registration?

The property owner must be physically present. The bank representative is not required if you have an exemption letter.

5. Can Reconveyance Deed be registered after 90 days?

No. If the deed’s date exceeds 90 days, the sub-registrar will not accept it. You need to approach the bank for a fresh Reconveyance Deed.

6. What are the government charges for Reconveyance in Karnataka?

- Stamp Duty – Rs.200

- Registration Fee – Rs.00

- Scanning Charges – Rs.50 per page

7. Can I authorize someone else to register the Reconveyance Deed?

Yes, you may issue a Power of Attorney (POA). Your POA holder can collect the documents and register the deed on your behalf.

8. How to confirm successful Reconveyance?

After registration, apply for the latest Encumbrance Certificate (EC). The EC should reflect your name as the owner and remove the bank’s name.

NEED ASSISTANCE?

We provide professional assistance with Reconveyance Deed registration in Bangalore & Mysore:

WhatsApp +91-9742479020 or email pgnproperties@gmail.com